A DCF calculator is a financial tool designed to compute the present value of an investment’s expected future cash flows. Its primary function is to help investors determine an asset’s intrinsic value by inputting key financial assumptions. You have a discount rate of 10% and an investment opportunity that would produce $100 per year for the following three years. Your goal is to calculate the value today—the present value—of this stream of future cash flows. Since money in the future is worth less than money today, you reduce the present value of each of these cash flows by your 10% discount rate.

Additional Considerations in DCF Analysis

Discounting cash flows is important because it takes into account the fact that money today is worth more than money in the future. Furthermore, future cash flows rely on a variety of factors, such as market demand, the status of the economy, technology, competition, and unforeseen threats or opportunities. Investors must understand this inherent drawback for their decision-making. The initial investment is $11 million, and the project will last for five years, with the following estimated cash flows per year. Firms and individuals conducting discounted cash flow analysis can benefit from the use of software.

Calculating Unlevered Free Cash Flows (FCF)

This formula uses a fixed trading multiple, which is a function of expected investor demand. Finding an appropriate multiple usually involves comparisons to similar companies that have exited and/or gone through funding rounds at similar growth stages, in similar market conditions. Industry average valuation multiples can also be used in a pinch—but keep in mind that these multiples tend to shift over time with investor demand, risk appetite, and the interest rate environment. The forecast period refers to the length of time that you can reasonably estimate the cash flows from a project. For debt-funded companies, WACC may simply be the average cost of servicing that debt. For equity-funded companies, it’s the average cost of equity (or the expected/demanded return by shareholders).

Company

To determine the changes in working capital in the projection period, very often we will need to do a forecast by ourselves if we don’t have a projected balance sheet. Common techniques in forecasting the working capital includes benchmarking to the revenue and turnover days etc. For the sake of time we are not going to cover how to define working capital and forecasting method in this article. In the sample forecast, we have already projected the working capital balance for you. Very often, when your business is growing, you will need more inventory and operating cash.

- As an equity analyst, rather than making our own assumptions, we can use a DCF model to ask the question “what has to be true for the current share price to be correct?

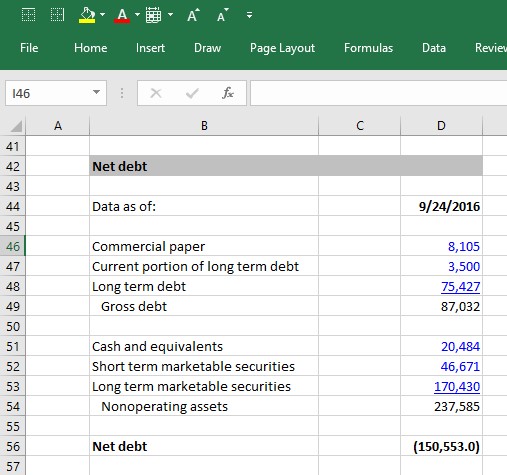

- That’s because they are mostly comprised of cash and liquid investments that companies generally can mark up to fair value.

- There are two kinds of cash flows when it comes to DCF, one is free cash flow to firm (FCFF) and the other is free cash flow to equity (FCFE).

- An alternative to the perpetuity method for Terminal value is to use an exit multiple after 5 years.

- Also, you should not add back the Operating Lease Depreciation or Amortization because in this case, it represents part of an actual cash expense.

Cognitive biases and some good and bad investment habits

A discounted cash flow (DCF) model is a financial model used to value companies by discounting their future cash flow to the present value. In this guide, we’ll provide you with an overview of the components of a DCF model. This will serve as a reference tool for before or after our financial modeling course where we build a DCF model on public company.

Also, the DCF approach values a business at a single point in time (i.e., the Valuation Date). This metric represents the percentage of revenue that translates into profit. By inputting dcf model steps expected net profit margins, users can accurately estimate future profitability. The discount rate is a key input in the DCF model and has a big impact on the results.

So, if the assumed growth rate during the forecast period was 9%, then the perpetual growth rate would also be 9%. For solely debt-funded companies, WACC is mostly influenced by borrowing costs (which means it’s also at the mercy of inflation and changing interest rates). For equity-funded firms, the cost of equity is largely based on investor demand and expectations of return. For companies with hybrid funding, WACC takes a weighted average of the two. In the SaaS industry, growth rates tend to be higher closer to launch, when the annual rate of return (ARR) is relatively low. For instance, SaaS firms with an ARR of under $1 million had a median growth rate of around 100%, compared to just 40% for firms with ARR in the $3 to $5 million range.

The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. The CAPM is used to estimate the required rate of return for an investment. Another challenge when using the DCF model is estimating the correct discount rate to use. Much like any other valuation method, the DCF model was designed for a specific application with certain assumptions, which means it has a few limitations that you need to be aware of. In the case of a merger, the DCF model is used to determine the value of each company and how much they should be worth together.

If it does, you need to re-think your assumptions or extend the analysis. The Discount Rate is around 4.0% with this approach (assuming ~90% Equity and ~10% Debt for Walmart), close to the 4.37% in the full model. For example, it would be highly unusual if the Change in Working Capital represented 50% of a company’s UFCF. When creative this step-by-step guide, we have tried to makeit as clear as possible. But there are a lot more factors to consider in thereal world and this guide alone may not be able to solve all the issues you couldface in doing a DCF. If you need more help, you can always leave us comment orsend us your questions, we will get back to you as soon as possible.

The firm is considering whether or not the capital expenditure is worthwhile. A SaaS firm is investing $3 million in a project to launch a new paid upgrade feature to an existing offering. The firm chooses a 5-year forecast period as a reasonable length to accurately forecast returns. To find FCF for future years, simply multiply the FCF from the previous year by the expected growth rate.

![deco world sarı[1]-1-1](https://decoworld.com.tr/wp-content/uploads/elementor/thumbs/deco-world-sari1-1-1-qu92y56ep1hs9qpmnfo1mvtj8pqjkl3h87s5k0nama.png "deco world sarı[1]-1-1")